📅 Thursday, April 25th, 2024

I know not age, nor weariness nor defeat.

— Rose Kennedy

MGT011A Lecture: Ch. 3 problems, Ch. 4 notes

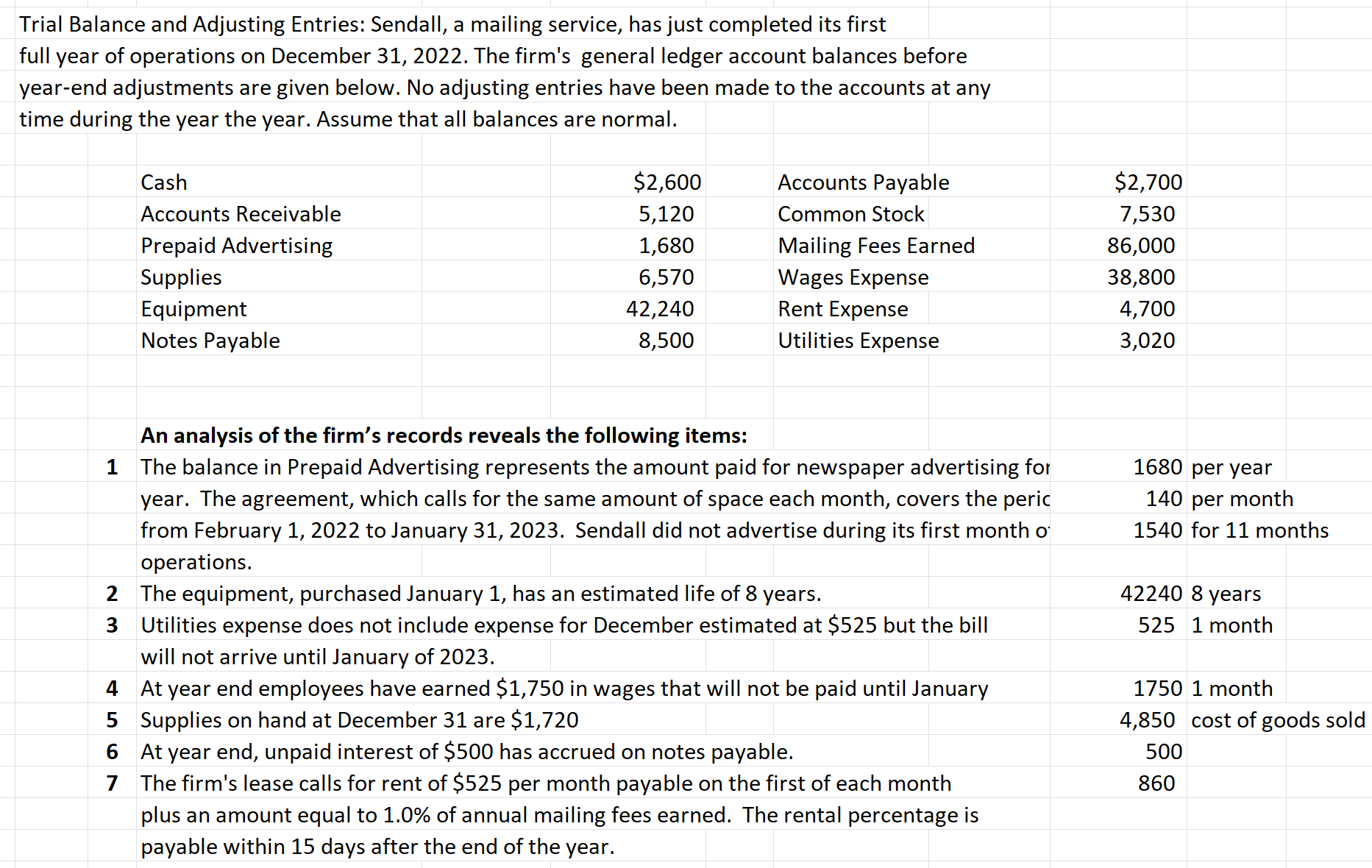

Ch. 3 In-Class Problem 1

Firm records:

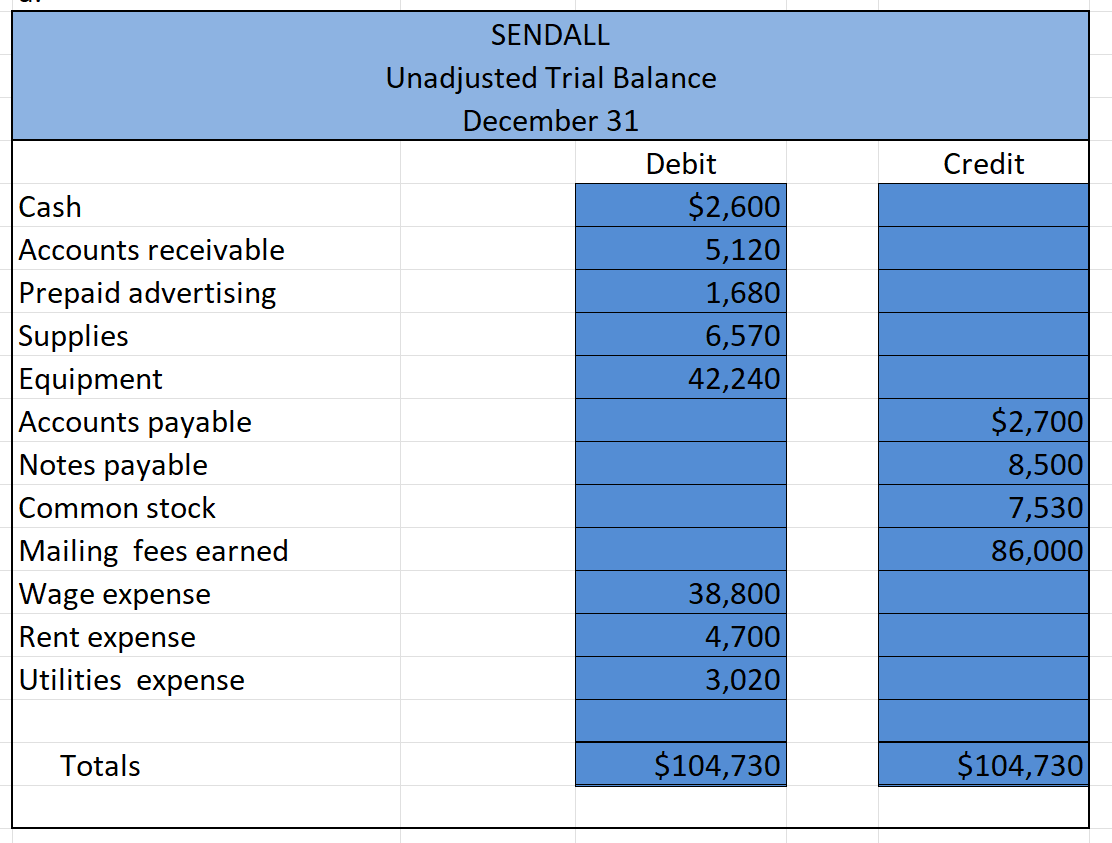

Unadjusted trial balance:

Unadjusted trial balance:

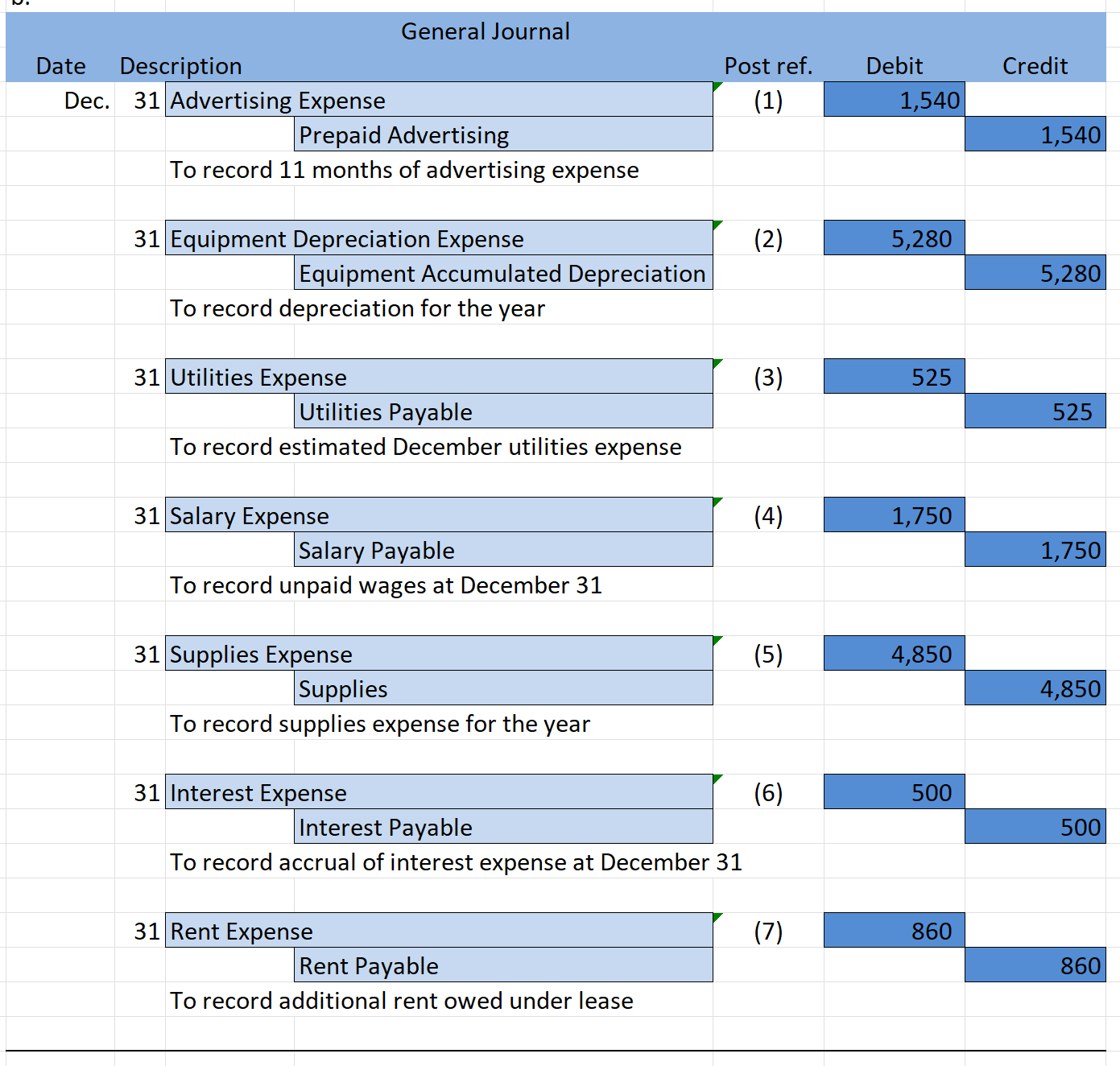

General journal:

General journal:

Important concepts for ch. 3 quiz: how to journalize adjusting entries, esp. depreciation expense.

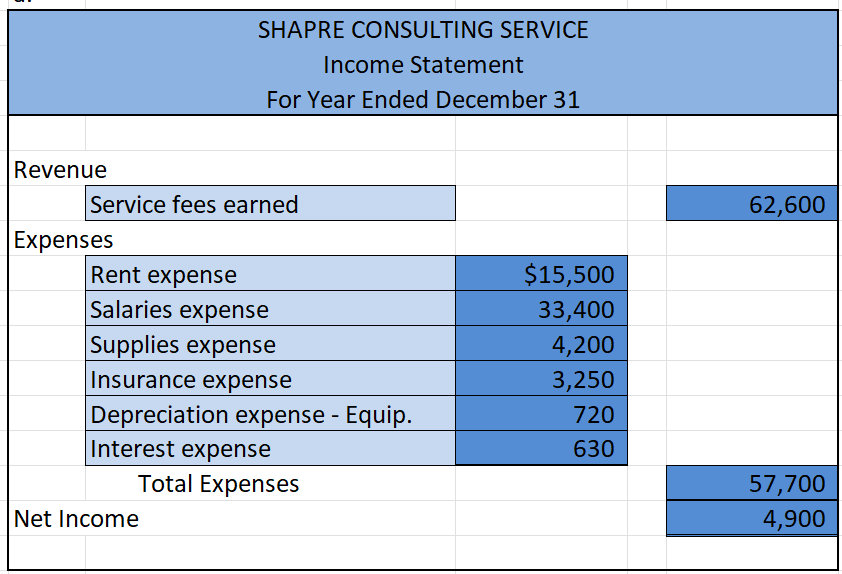

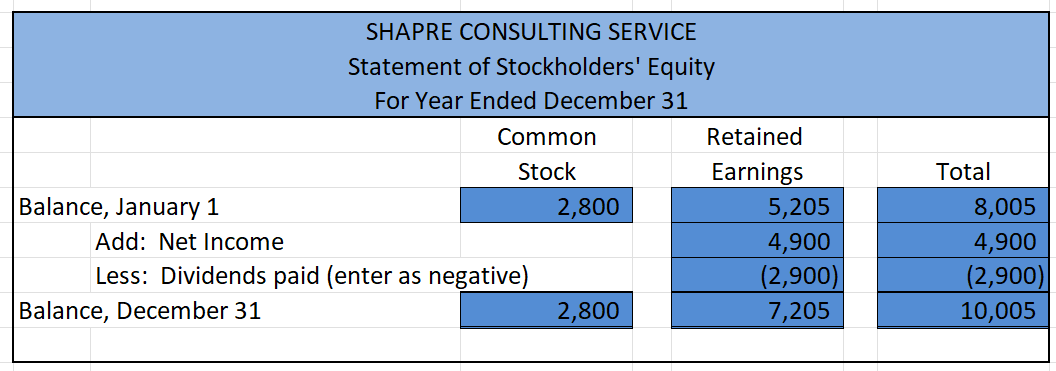

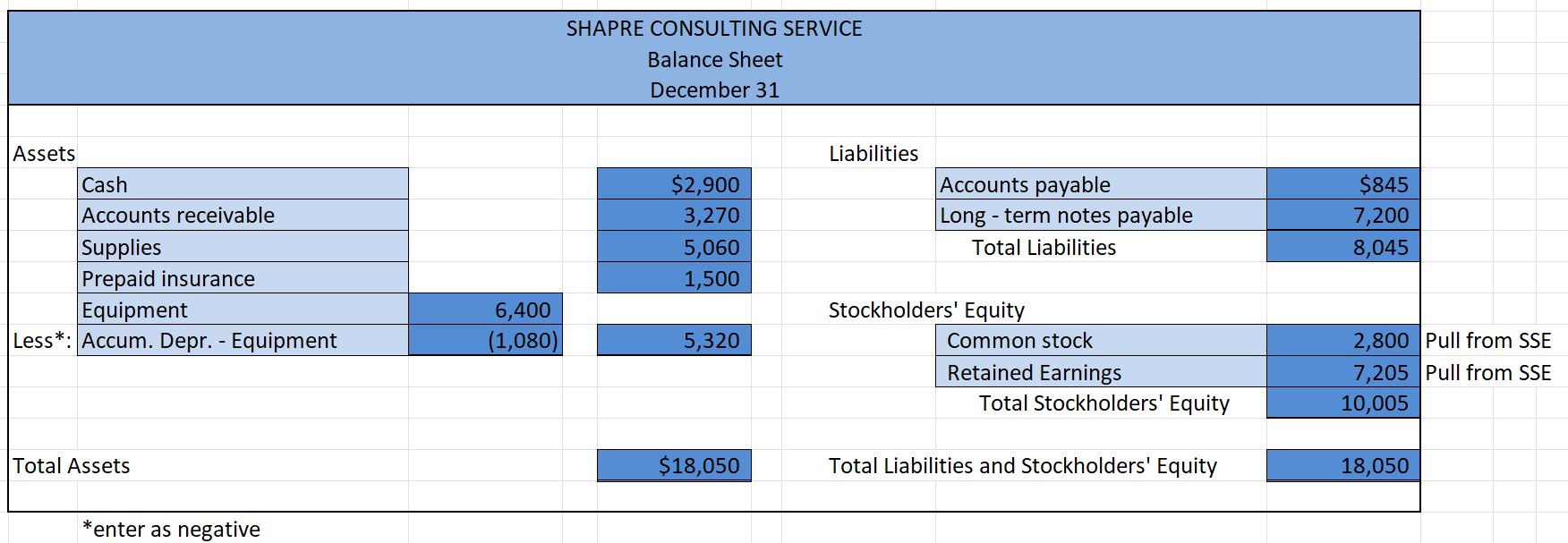

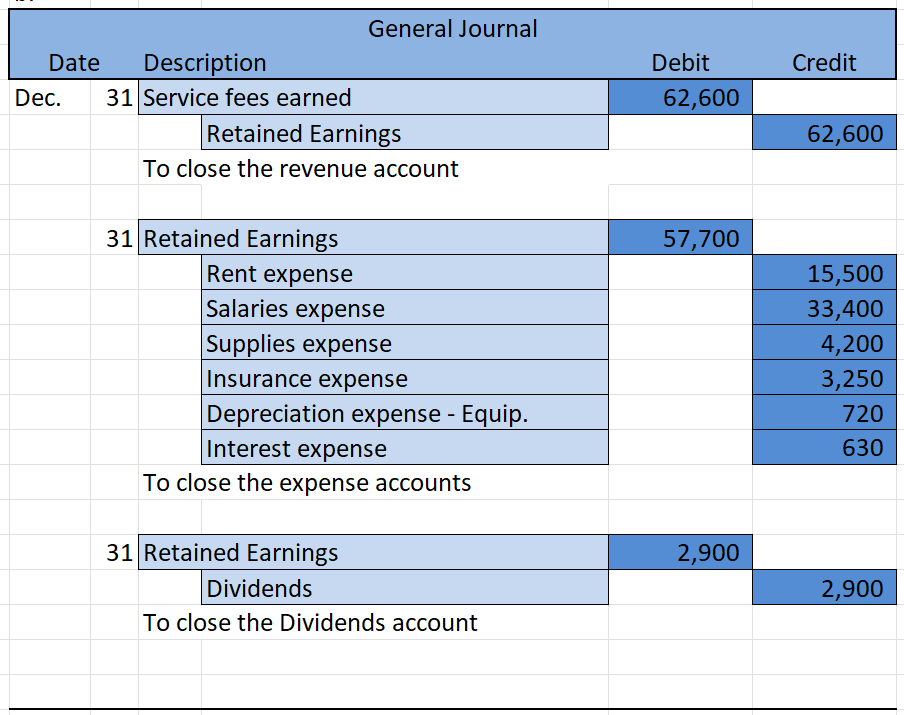

Ch. 3 In-Class Problem 2

closing entries (remember to use the actual account name, not just “Revenue”):

Remember which accounts to close (revenue, expense, dividends) and how to journalize the closing entries.

Remember which accounts to close (revenue, expense, dividends) and how to journalize the closing entries.

Ch. 4 notes

- operating cycle: average period of time to buy materials, produce product, then sell and receive revenue for it; typically less than a year

- current asset: assets that are expected to be liquidated, or consumed within the company’s operating cycle or 1 year, whichever is longer

- assets are listed in order of expected liquidity (from most to least):

- cash

- short-term investments (e.g., money market?)

- accounts receivable (A/R)

- inventory

- other current assets

- assets are listed in order of expected liquidity (from most to least):

- noncurrent assets: assets that the company does not intend to liquidate or consume during the operating cycle or one year, whichever is longer

- examples

- Property, Plant, and Equipment (PP&E): land, buildings, equipment, vehicles, furniture & fixture

- intangible assets: non-physical assets such as brand names, copyrights, patents, trademarks

- other long-term assets

- examples

- current liability: obligations to be settled within a year or an operating cycle, whichever is longer

- liabilities are listed in order of maturity

- accounts payable

- accrued expenses

- short-term notes payable

- other current liabilities

- liabilities are listed in order of maturity

- long-term liability: obligations that don’t need to be paid within a year / operating cycle, whichever is shorter

- balance sheet in account form: very brief balance sheet (what we’ve been doing in the class, and we won’t make them anymore)

- classified balance sheet: balance sheet that divides current & noncurrent (long-term) assets or liabilities, which helps investors & banks see on whether the assets & liabilities affect the short-term